Under OECD Transfer Pricing Guidelines Chapter I, Paragraphs 1.51 through 1.106, the functional profile of each entity determines its appropriate return. A full-risk manufacturer with significant functions and assets is entitled to a larger profit allocation than a limited-risk contract manufacturer that performs routine functions under a principal’s direction.

The functional analysis must describe actual operations — not the idealized structure described in legal agreements. If the two differ, the actual operations govern.

2. Economic Analysis and Method Selection — The Pricing Core

The economic analysis applies the selected transfer pricing method to establish an arm’s-length result. The method must be the best method under Treasury Regulation Section 1.482-1(c) — the one that provides the most reliable measure of an arm’s-length result given the facts and circumstances of the transaction.

The documentation must include a best-method analysis that identifies all applicable methods, explains the strengths and weaknesses of each, and demonstrates why the selected method is superior.

For the CPM (comparable profits method), the economic analysis identifies a set of comparable companies, calculates each comparable’s profit level indicator (operating margin, return on costs, or Berry ratio), derives an interquartile range, and compares the tested party’s actual result to that range.

For a CUP (comparable uncontrolled price), the analysis identifies comparable transactions and adjusts for material differences.

3. Benchmarking Study — Market Evidence for Arm’s-Length Pricing

The benchmarking study is the market evidence that supports the arm’s-length result. It identifies independent companies or transactions that are comparable to the tested party or the controlled transaction, and uses their financial results to establish an arm’s-length range.

The study must document: the search process used to identify comparables (database used, search criteria, acceptance and rejection criteria); the comparables selected and their financial data for the tested years; the adjustments made to improve comparability (working capital adjustments, functional adjustments, accounting adjustments); and the calculation of the arm’s-length range using the interquartile method.

Benchmarking data must be current — studies using comparables from prior years do not reflect current market conditions and may not satisfy the contemporaneous standard if the business environment has changed materially.

4. Intercompany Agreements — The Legal Framework

Intercompany agreements are a required component of penalty protection documentation under Treasury Regulation Section 1.6662-6(d). They define the legal terms of the transaction: the transfer pricing method selected, the resulting price or margin range, the risk allocation between parties, the payment schedule, and the conditions under which the agreement may be amended.

The agreement must be consistent with the functional analysis in the transfer pricing study — if the study designates an entity as limited-risk, the agreement must allocate limited risk to that entity. Agreements that conflict with the study are treated as evidence of bad faith by the IRS.

Agreements must be executed before the transactions they govern — a December agreement does not apply to January-through-November transactions.

5. Financial Data and Supporting Records

The documentation must include the financial data underlying the analysis: actual revenue, costs, and profit margins for each entity involved in the controlled transaction for the tested year; segmented financial data showing the results of the controlled transaction separately from other business activities if the entity engages in multiple transaction types; and the financial data used to calculate the comparable companies’ profit level indicators.

Supporting records include: the database search output showing comparables identified and rejected; the financial statements of comparable companies; any transfer pricing adjustments made to the tested party’s or comparables’ financial data; and any projections used in an income-based analysis.

These supporting records must be preserved in a form that can be produced to the IRS within 30 days of request.

How Do OECD BEPS Action 13 Documentation Requirements Apply?

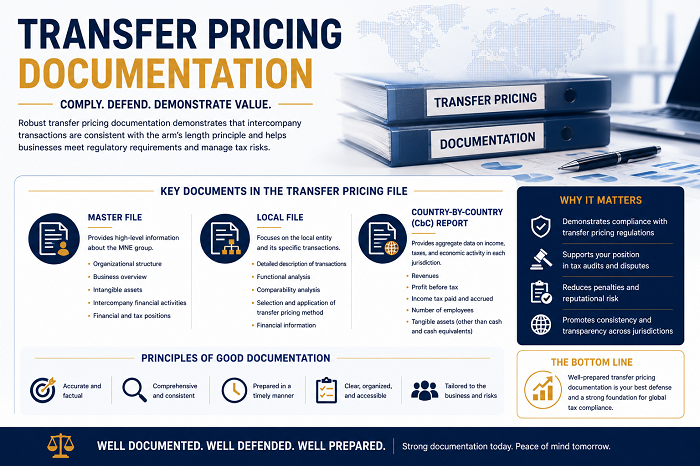

For multinational groups with operations in countries that have adopted OECD BEPS Action 13, the documentation requirement extends beyond the U.S. contemporaneous study to include a three-tier documentation framework: a Master File providing a high-level overview of the group’s global operations, transfer pricing policies, and intangible property; a Local File providing entity-specific documentation for each jurisdiction, including a description of each controlled transaction, the method selected, and the benchmarking support; and a Country-by-Country Report (CbCR) providing jurisdiction-by-jurisdiction data on revenue, profit, taxes, employees, and assets.

| Document |

Content Summary |

Who Files It |

Revenue Threshold |

Due Date |

| U.S. contemporaneous documentation (Treas. Reg. §1.6662-6(d)) |

9-element study: functional analysis, method selection, benchmarking, comparables, financial data, agreements

|

U.S. taxpayer |

All taxpayers with IRC §482 transactions |

Must exist at return filing; produced within 30 days of IRS request

|

| OECD Master File (BEPS Action 13) |

Group structure, global TP policies, IP ownership, global financing, consolidated financials

|

Ultimate parent entity or designated filer |

€750M+ (varies by country) |

Generally due with the corporate income tax return in each jurisdiction

|

| OECD Local File (BEPS Action 13) |

Entity-specific functional analysis, description of each controlled transaction, method selection, benchmarking

|

Each local entity in each jurisdiction |

Varies by country; many set a transaction-level threshold

|

Generally due with local corporate income tax return

|

| Country-by-Country Report / Form 8975 (U.S.) |

Jurisdiction-level: revenue, pre-tax profit, taxes paid/accrued, employees, tangible assets for each entity

|

Ultimate parent of U.S. MNE group |

$850M+ prior-year annual revenue (26 C.F.R. §1.6038-4)

|

12 months after close of reporting fiscal year; filed with Form 1120

|

| Intercompany agreements |

Transaction terms, pricing method, risk allocation, payment terms, amendment provisions

|

U.S. taxpayer and related parties |

All intercompany transactions; required component of Treas. Reg. §1.6662-6(d)

|

Must exist before transactions; produced within 30 days of IRS request

|

What Documentation Failures Most Commonly Lead to Penalties?

| Documentation Failure |

Why It Eliminates Penalty Protection |

IRS Consequence |

|

Documentation prepared after audit begins (not contemporaneous)

|

Treas. Reg. §1.6662-6(d) explicitly requires documentation to be in existence at filing; post-filing documentation is not “contemporaneous”

|

Penalty applied automatically; post-filing documentation considered only for reasonable cause argument, which rarely succeeds without pre-filing documentation

|

|

Functional analysis describes idealized structure, not actual operations

|

OECD accurate delineation standard and U.S. substance-over-form doctrine look to actual conduct; documentation that does not reflect reality is unreliable

|

IRS performs independent functional analysis based on actual operations; typically produces a less favorable result

|

|

Benchmarking study uses outdated or non-comparable companies

|

Stale comparables may not reflect current market conditions; non-comparable companies produce an indefensible arm’s-length range

|

IRS uses its own current comparable set; resulting arm’s-length range may produce a larger adjustment

|

|

Study covers only some intercompany transactions

|

Transactions not covered by documentation are treated as undocumented; documentation-triggered penalty applies to those transactions

|

Penalty applies to undocumented transactions regardless of whether the documented transactions are acceptable

|

|

Financial data in study does not match return data

|

Inconsistency between study financials and return financials is evidence of unreliability; IRS treats study as untrustworthy

|

IRS may disregard study entirely; penalty protection lost for all transactions covered by the study

|

|

Documentation not produced within 30 days of IRS IDR

|

Treas. Reg. §1.6662-6(d)(3) requires production within 30 days; late production is treated the same as no documentation for penalty purposes

|

Documentation-triggered penalty applied; 30-day deadline is not extendable without IRS consent

|

30-DAY PRODUCTION REQUIREMENT

The 30-day documentation production deadline under Treasury Regulation Section 1.6662-6(d)(3) is one of the most operationally important requirements in transfer pricing compliance. Companies that have a complete, current transfer pricing study stored in an accessible, centralized location can meet this deadline routinely. Companies that do not maintain organized documentation frequently miss it, converting a defensible transfer pricing position into an automatic penalty.