Setting intercompany transaction prices isn’t a one-size-fits-all exercise. The choice of

transfer pricing methods,

methodology and

techniques can make a meaningful difference in audit defence and tax outcomes. At WTP Advisors, we help you evaluate and implement the most appropriate method for your specific circumstances.

Why Methodology Matters

Tax authorities around the world require that related-party transactions be priced using methods that reflect arm’s-length arrangements. The method you select affects how comfortable you will be under review or audit. (

wtpadvisors.com) Picking the right transfer pricing method is fundamental to:

- Achieving a defensible result

- Minimising adjustment risk

- Aligning with functional, asset and risk profiles

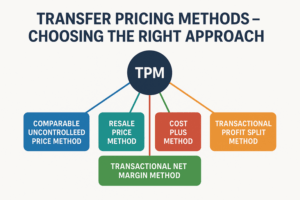

Common Transfer Pricing Methods

Here are some of the standard options:

- Comparable Uncontrolled Price (CUP) Method: Compare the internal transaction with similar uncontrolled transactions.

- Resale Price Method: Suitable for distributors; starts with resale margin and subtracts an appropriate mark-up.

- Cost Plus Method: Suitable for manufacturing or services; cost base plus arm’s-length mark-up.

- Transactional Net Margin Method (TNMM): Looks at net profit margin relative to a base (e.g., costs, sales) and compares to third-party benchmarks.

- Profit Split Method: Suitable when both parties contribute unique intangibles or perform significant functions; profits are split according to an economic rationale. (wtpadvisors.com)

Selecting the Right Technique

Choosing among these methods requires a structured methodology:

- Assess your functional profile (who does what, uses what assets, assumes what risks)

- Determine availability of reliable comparables (third-party transactions)

- Evaluate which method aligns with your facts and is acceptable in jurisdictions of interest

- Consider documentation burden and defence strength

WTP Advisors helps you carry out this assessment, select the technique that balances robustness and practicability, and structure your policy accordingly.

Advanced Techniques and Considerations

In more complex cases — for example intangibles, services, digital business models — you may need refined techniques:

- Profit-split variations tailored for integration of intangibles

- Hybrid models: combining cost-plus and TNMM or adjusting for risk profiles

- Use of benchmarking databases, statistical adjustments and modelling

- Scenario modelling to test sensitivities and audit risk

WTP Advisors’ team brings sophisticated technical tools and documented method-frameworks to these advanced issues.

Why Partner with WTP Advisors

Because selecting the wrong method or applying it poorly can cost you — in audits, adjustments, penalties or lost planning opportunities. WTP Advisors offers:

- Proven experience with multinational clients and multiple jurisdictions

- Strong documentation support and audit-readiness frameworks (wtpadvisors.com)

- A methodology-first mindset: not just doing the work, but structuring it for defensibility

If your next transfer pricing review or redesign is approaching, this is the time to evaluate your method choice carefully.

Conclusion

The right transfer pricing method is both analytical and strategic: matching facts with technique, aligning with value-creation, and preparing for tax authority scrutiny. With the guidance of WTP Advisors, you can build a method-selection process that strengthens your international tax posture.