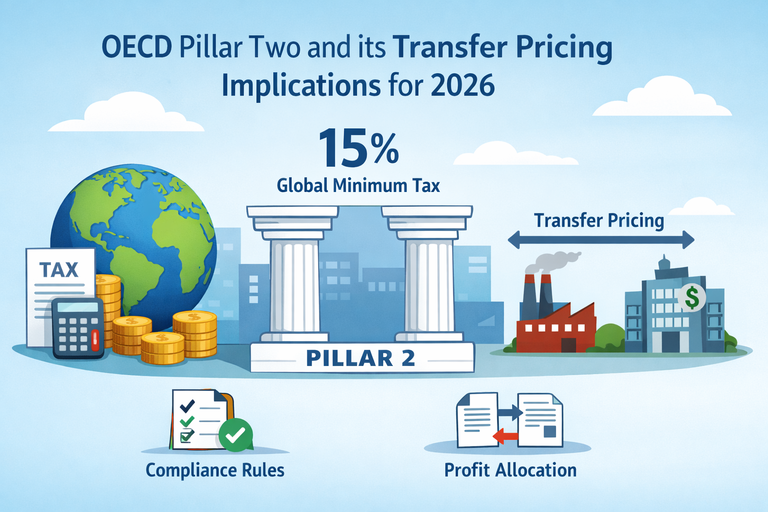

The global tax landscape is undergoing a significant transformation with the implementation of the OECD’s Pillar Two initiative, also known as the Global Anti-Base Erosion (GloBE) rules. These rules aim to ensure that multinational enterprises (MNEs) pay a minimum effective tax rate of 15% on their profits in every jurisdiction where they operate. While primarily… Continue reading OECD Pillar Two and its Transfer Pricing Implications for 2026

Transfer Pricing for Marketing and Distribution Activities: Optimizing Value Chains in 2026

Marketing and distribution activities are crucial components of a multinational enterprise’s (MNE) value chain, directly impacting sales, brand recognition, and market penetration. However, the transfer pricing of these activities, particularly the remuneration of distributors and the allocation of marketing intangibles, remains a complex and frequently audited area. In 2026, MNEs must carefully structure and price… Continue reading Transfer Pricing for Marketing and Distribution Activities: Optimizing Value Chains in 2026