The landscape of transfer pricing is undergoing a significant transformation driven by rapid technological advancements. In 2026, multinational enterprises (MNEs) are increasingly leveraging digitalization, including artificial intelligence (AI), blockchain, and advanced data analytics, to enhance the efficiency, accuracy, and compliance of their transfer pricing processes. This shift is not merely about automation; it’s about fundamentally… Continue reading Digitalization of Transfer Pricing: Leveraging Technology in 2026

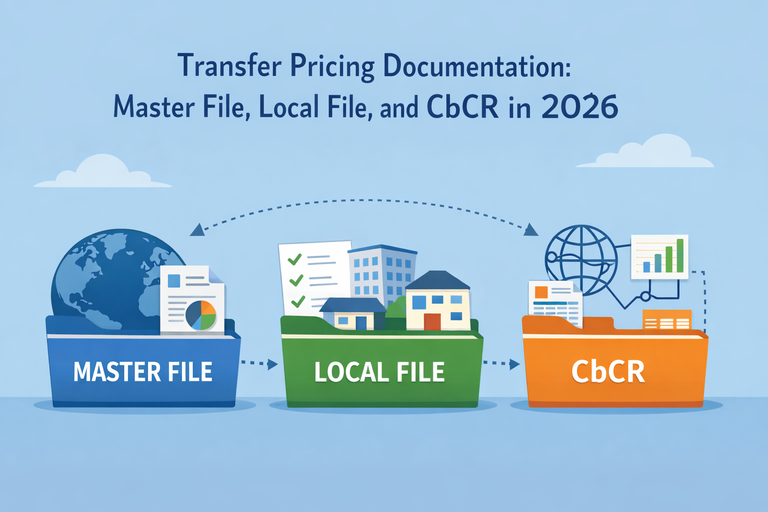

Transfer Pricing Documentation: Master File, Local File, and CbCR in 2026

Robust transfer pricing documentation is the cornerstone of compliance for multinational enterprises (MNEs). It serves as the primary means to demonstrate that intercompany transactions are conducted at arm’s length and to mitigate the risk of transfer pricing adjustments and penalties during tax audits. In 2026, MNEs continue to navigate the three-tiered documentation structure introduced by… Continue reading Transfer Pricing Documentation: Master File, Local File, and CbCR in 2026